Understanding Your Health Insurance Card: A Step-by-Step Guide

Navigating the world of health insurance can feel overwhelming, but one small piece of plastic (or digital equivalent) holds the key to unlocking your coverage: your insurance card. Provided by your health plan, this card is your go-to reference for everything from doctor visits to prescription pickups. Whether it’s tucked in your wallet or saved on your phone, understanding its details can save you time, money, and stress. In this article, we’ll break down the typical elements of a health insurance card, using insights from resources like the Centers for Medicare & Medicaid Services (CMS). Let’s demystify it together.

Why Your Insurance Card Matters

Your health plan likely sent you an insurance card shortly after enrollment. It’s not just a formality—it’s essential for providers to bill correctly and for you to access care. If you haven’t received one or can’t make sense of it, contact your plan immediately. Some plans offer digital versions via apps or portals, but the information remains the same. Cards vary by insurer, but they generally include key details about you, your coverage, and how to get help.

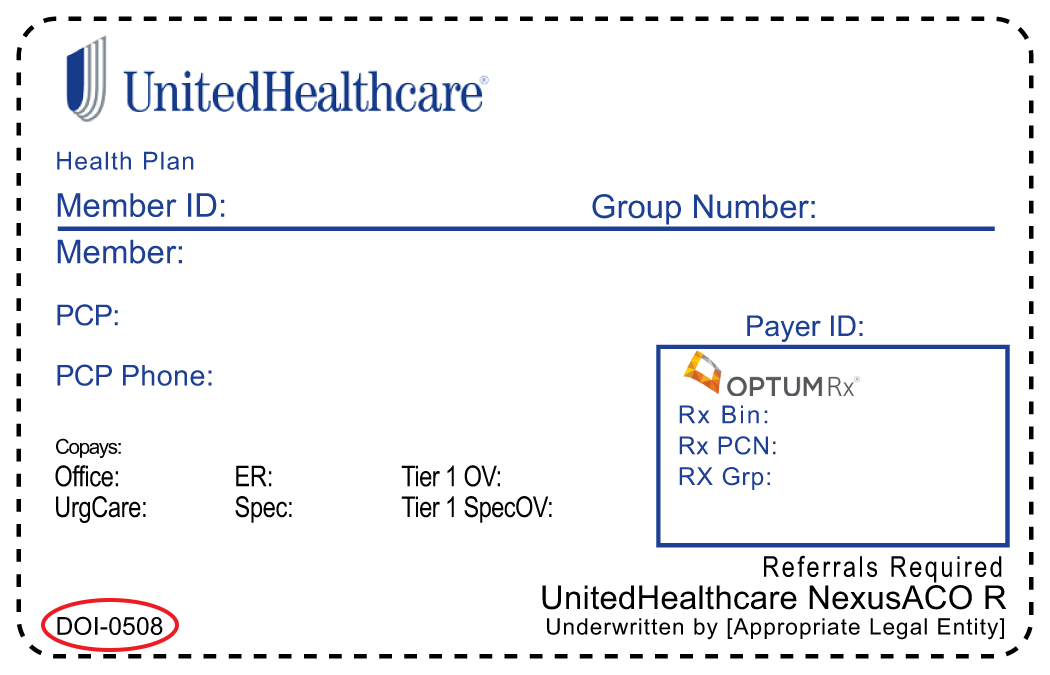

Breaking Down the Key Elements

Most insurance cards feature a standard set of information, often labeled for clarity. We’ll walk through each one, explaining what it means and why it’s important. Refer to the numbered sections on your own card as you read.

1. Member NameThis is straightforward: your full name as registered with the plan. It’s printed prominently to confirm the card belongs to you. Double-check for accuracy—if there’s a typo, notify your plan to avoid billing issues.

2. Member Number

Think of this as your unique identifier, like a social security number for your health plan. It’s used by providers to submit claims and verify eligibility. Family members on the same plan might have similar numbers, so keep track of who’s who. Example: XXX XXX XXXX.

3. Group Number

This code tracks the specific benefits tied to your employer’s group plan or individual policy. It’s crucial for providers to know exactly what your coverage entails, such as deductibles or covered services.

4. Copayments (Copays)

These are the fixed amounts you pay out-of-pocket for common services. Your card might list:

- Primary Care Physician (PCP) Copay: e.g., $15.00 for a routine check-up.

- Specialist Copay: e.g., $25.00 for seeing a specialist.

- Emergency Room Copay: e.g., $25.00 for ER visits. Knowing these upfront helps you budget for healthcare.

5. Phone Numbers

Your lifeline for questions! This includes customer service lines for finding in-network providers, checking coverage details, or resolving claims. Example: Member Service at 800-XXX-XXXX. Don’t hesitate to call—it’s better to ask than assume.

6. Plan Type

Labels like HMO (Health Maintenance Organization) or PPO (Preferred Provider Organization) indicate your network structure. HMOs often require referrals and stick to in-network providers for lower costs, while PPOs offer more flexibility but higher out-of-network fees. This tells you how to choose doctors without surprise bills. Example: Plan Type 134, effective from 1/1/21.

7. Prescription Copayments

Similar to service copays, these outline costs for medications:

- Generic: e.g., $15.00.

- Name Brand: e.g., $25.00. Look for a Prescription Group Number (e.g., 123456789) to use at pharmacies.

8. Pricing Information

Newer cards (often on the back) must include details like deductibles (what you pay before insurance kicks in) and out-of-pocket maximums (your annual spending cap). There’s usually a phone number or website for more info. This transparency helps you plan financially.

Tips for Using Your Card Effectively

- Keep it safe and accessible: Snap a photo on your phone or store it in a secure app.

- Understand networks: Stick to “in-network” providers to minimize costs—your plan type guides this.

- Update as needed: Life changes like marriage or a new job might require a new card.

- No card? No problem: Contact your plan for alternatives, like printable versions.

- Digital trends: Many insurers now offer electronic cards with QR codes for quick scans at appointments.

By familiarizing yourself with these elements, you’ll feel more empowered in managing your health coverage. If you’re in Brooksville, Florida, or elsewhere, resources like go.cms.gov/c2c provide additional support. Remember, this guide is based on general CMS information—always refer to your specific plan documents for personalized details. If you have questions about your policy, reach out to your insurer today.

If you have any questions on understanding your insurance card, I’m always here to help. Give me a call at 813-517-7953, email RikkiToppsInsurance@gmail.com.

Insurance, made easy and caring – that’s the Rikki way!

Don’t Let Insurance Get Tricky, Call Rikki!Still have questions?

Feel free to contact me at RikkiToppsInsurance@gmail.com or by phone at 813.517.7953, and I’ll be happy to answer any other questions you have. (License #W282762)(This article is for educational purposes and not a substitute for professional advice. Source: CMS Publication #11818, Revised May 2022.)